At the fourth in a series of eight webinars hosted by Student Financial Support, financial educator Shahar Ziv explained the basics of credits and how to use credit cards to your greatest advantage. Some top insights from the session include:

- Your credit score is your financial GPA. It takes the information from your credit report (the financial equivalent of your academic transcript) and turns it into a number. Lenders and other entities (like some employers, landlords, and licensing boards) use this number to gauge your risk of defaulting on a loan, the same way that a grad school admissions counselor uses your GPA to judge how well you’d perform in their program. All credit scores are three-digit numbers between 300 and 850. A higher credit score will get you better terms on loans, in the form of more money and/or lower interest rates.

- You can check your credit report for free. You are legally entitled to one free report per year from each of the three credit reporting bureaus (Experian, TransUnion, and Equifax). Start at AnnualCreditReport.com (NOT FreeCreditReport.com) to get this information. You can stagger the three reports across the year and check your report once every four months. Knowledge is power.

- Credit can help you, but it can also hurt you. Credit can easily facilitate overspending. In the case of credit cards specifically, the debt often has double-digit interest rates, which means you end up paying far more for your purchases over the course of the loan than if you’d used cash at the time of purchase. (The same goes for “Buy Now Pay Later” checkout options.) Studies show that credit card debt increases stress and anxiety for many people.

- Debit cards ≠ credit cards. The physical card (or digital apps) may look the same, but they work differently.

- With debit cards, there’s no application process; you just get one when you open an account at a bank or credit union. When you use a debit card, the money is immediately deducted from the cash in your checking account. If there isn’t sufficient money in the account, the purchase won’t go through. Because you can’t spend more than you have, debit card accounts can’t accrue interest or late fees. On the negative side, debit cards don’t help to build your credit history.

- By contrast, credit cards require an application process. If you are approved, the credit available to you is essentially a loan. At the end of each month, you must make at least a minimum payment on that loan or you will incur late fees, plus interest on the outstanding balancea. Credit cards offer certain security benefits that debit cards do not, and using one and paying it off in a timely fashion can help to build your credit history. Additionally, many credit cards come with rewards in the form of reimbursement and/or discounts (although check No. 9 on this list before you get too excited about rewards).

- Don’t fall into the “minimum payment” trap; aim to pay off your credit card balance in full every single month. Credit card minimum payments are calculated as a percentage of your outstanding balance, usually 1-3%. Paying only the minimum amount is less out of pocket in the short term, because it’s a smaller amount than the full balance and you’ll avoid late fees. But paying off the debt will ultimately cost you far more over time due to the high interest rates (12-20%) that you’ll be charged over the course of the loan. The example below illustrates how a lower minimum payment adds up to more over the life of the loan.

Card A Card B Balance $5,000 $5,000 Interest Rate 18% 18% Minimum Payment 3% 4% Total Interest $4,567 $2,808 Years to Repay 16 11 - It’s fine (and even beneficial) to pay off credit cards early. There’s a persistent financial myth that paying off credit cards (or other loans) early will hurt your credit score. It’s not true. Showing you paid off debt is the important part, and doing so on a shorter timeline is fine and can even increase your score.

- When selecting a credit card, consider the interest rateb, annual feec, additional feesd, rewards, and other benefits when choosing a credit card. CreditKarma and NerdWallet can be good tools to figure out what works best for you, your budget, and your financial goals. Don’t get caught up in the “total value” of a card; its value to you is what’s most important and that will differ for each person.

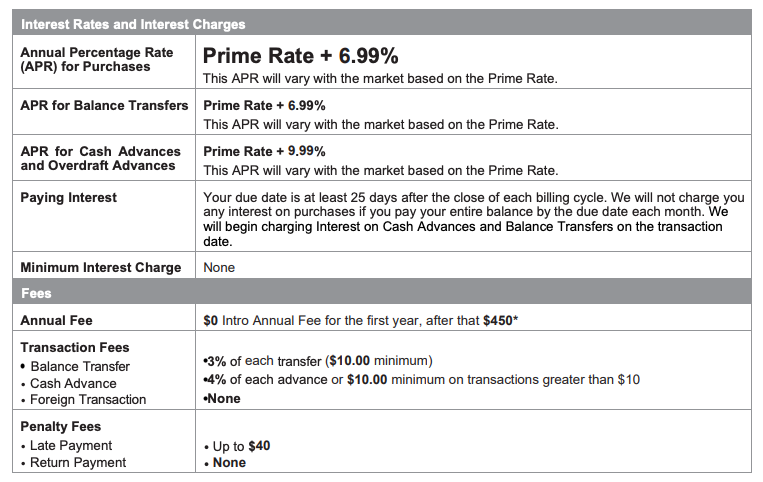

- Look for the “Schumer Box” on the first page of any credit card agreement or statement. It’s a legally required table that details all the basic rates and fees in a straightforward way. The box gets its name from New York Sen. Chuck Schumer who advocated for transparency in credit card terms. It usually looks something like this:

Source: Consumer Financial Protection Bureau - Reward cards are only useful if you are consistently paying off your balance every month. The very best reward programs offer up to about 5% cashback (or an equivalent amount in other rewards). Most credit card interest rates are between 12-20%. 5% is less than 12%, and it’s way less than 20%. If you aren’t consistently paying off your balance, you’re on the wrong side of that deal.

- iGrad is free to Hopkins students and has modules on credit. Check out this online financial education resource if you want to learn more.

The full video is available below. Don’t forget to register for the next installment in the series.

a. An outstanding balance is the amount that you owe. If you had a $1000 bill and paid $100 on that bill, your outstanding balance would be $900.

b. An interest rate is the price you pay to borrow money. Here’s a very simplified example: If you borrow $1000 at a 1% interest rate, you’d owe your lender $1010 (the original amount plus 1%) at the end of the loan. If you borrow $1000 at a 10% interest rate, you’d owe your lender $1100 at the end of the loan.

c. Some credit card companies charge an annual flat fee to card holders. Even if you never use the card, you will still owe the annual fee.

d. Some credit card agreements have fees for specific types of transactions. You might pay additional fees on foreign transactions, cash advances or late payments. It varies by the company, the type of card, and the card holder. Read your agreement carefully to make sure you understand what fees may be imposed.